On a Tuesday morning in Frankfurt, a senior credit officer at a major European bank stares at a spreadsheet that refuses to tell the whole truth. Outside, the rain slickens the cobblestones of the Finanzplatz, but inside the glass tower, the atmosphere is dry, climate-controlled, and increasingly anxious. He is looking at the "missing" loans.

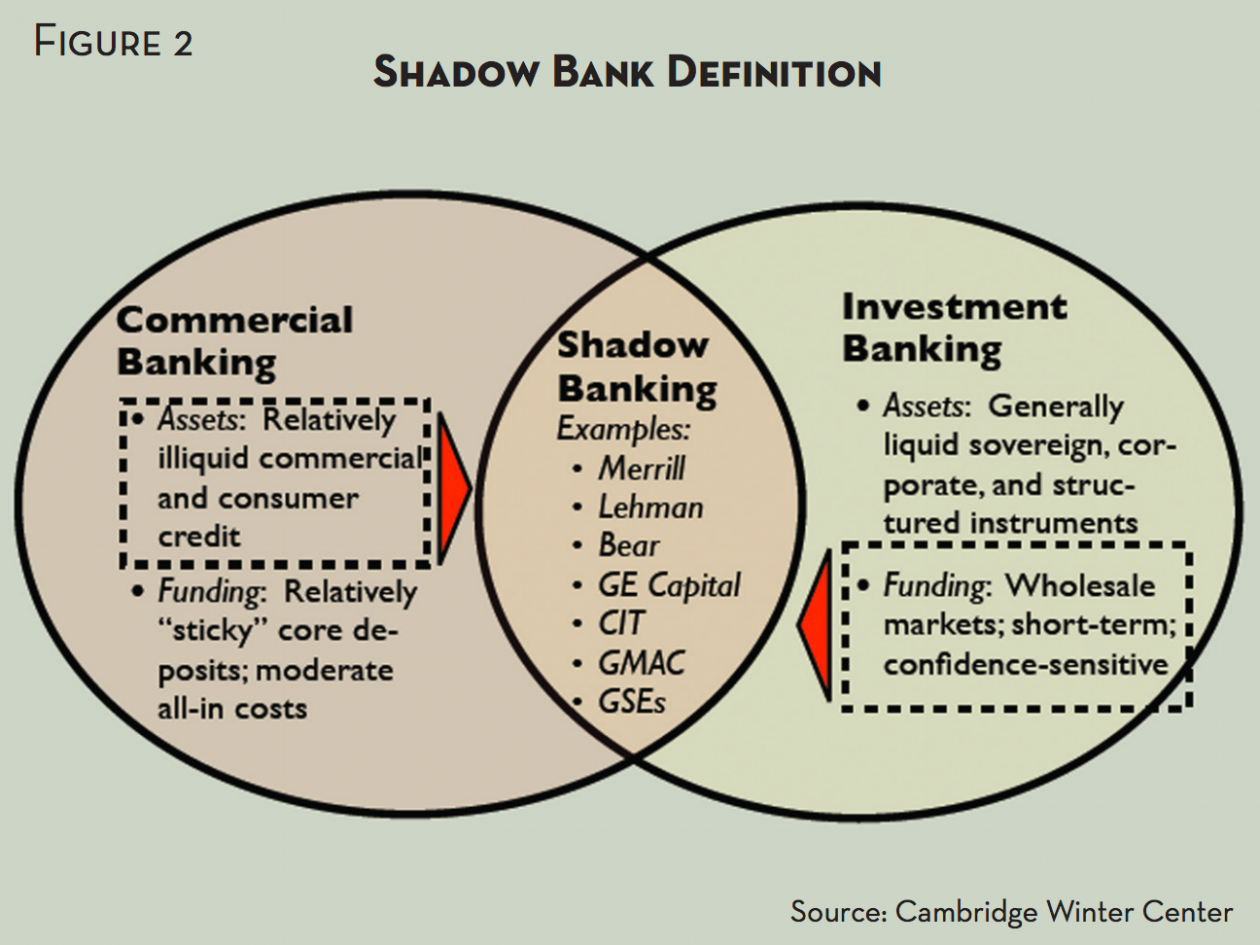

For decades, if a medium-sized German manufacturer or a French tech firm needed a hundred million euros to expand, they walked through his front door. They shook hands. They signed papers that the bank held in its vaults. Today, those companies are walking past the bank entirely. They are heading into the discreet, plush offices of private credit firms—the "shadow banks" that have quietly built a multi-trillion-dollar parallel universe.

As the European earnings season begins, the CEOs of Deutsche Bank, BNP Paribas, and UniCredit are preparing to stand before microphones. They will talk about interest margins and capital ratios. But the ghost at the feast is the money they can no longer see.

The Handshake in the Dark

To understand why this matters to someone who has never heard of a "collateralized loan obligation," consider a hypothetical baker named Marc in Lyon.

Marc needs to modernize his industrial ovens. In 2014, he would have gone to his local bank. The bank, regulated by the European Central Bank (ECB), would have scrutinized his flour invoices for six months before saying yes. It was slow, but it was transparent.

Now, Marc meets a private debt fund manager. The deal is done in three weeks. No public filings. No heavy-handed regulators breathing down their necks. The fund manager isn't using deposits from grandmothers' savings accounts; they are using "dry powder" from pension funds and sovereign wealth entities.

This is the allure of private credit. It is fast. It is flexible. It is also, by design, invisible.

The problem for the European banking system is that these invisible deals are cannibalizing the very core of their business model. When the economy is booming, everyone wins. The baker gets his ovens, the fund gets its high interest, and the banks... well, the banks watch from the sidelines, feeling a bit lighter in the pocket but safe from risk.

But the wind is changing.

The Ticking of the Hidden Clock

The European economy is currently a collection of contradictions. Inflation is cooling, yet the cost of living remains a weight on the chest of the average consumer. Interest rates are high, which usually means banks make more money on the loans they have. This is the "net interest income" boost that has propped up bank stocks for the last two years.

However, that boost is a sugar high.

The real danger lies in the "credit quality" of those who couldn't get bank loans and turned to the private market instead. If those companies start to fail because they cannot keep up with high interest payments, the contagion doesn't stay in the shadows. It leaks.

Banks are linked to these private credit funds through complex webs of financing. They provide the "leverage" that these funds use to juice their returns. Think of it as a house of cards where the bottom floor is built of solid stone (the banks), but the upper floors are made of mist (private credit). If the mist evaporates, the stone floor still feels the vibration of the fall.

Consider the "syndicated loan" market. This was once the bread and butter of European investment banking. Banks would underwrite a massive loan and then sell pieces of it to other investors. It was a communal way of spreading risk. Today, that market is emaciated. Private credit has snatched the best deals away, leaving the banks with the leftovers—the companies too risky even for the "risk-takers," or the ones too small to bother with.

The Earnings Whisper

As the quarterly results trickle out, analysts are hunting for a specific phrase: "Provisions for credit losses."

This is the money banks set aside because they expect people not to pay them back. It is a confession. If these numbers spike, it tells us that the "shadow" world is starting to bleed into the light.

There is a quiet tension in the way bank executives answer questions about competition. They claim they aren't worried. They say they are being "disciplined." But discipline is often just another word for "we are losing market share and don't know how to stop it."

The European Central Bank is watching. They recently began a "thematic review" of how banks are exposed to private credit. In the language of central bankers, "thematic review" is code for "we are worried this might blow up, and we want to know whose fault it will be."

They are looking for the "hidden leverage." It’s the money borrowed to borrow more money.

The Human Cost of the Invisible

Why should a schoolteacher in Madrid or a nurse in Milan care about this?

Because banking crises in Europe are never just about banks. They are about the "transmission mechanism." When banks get scared—whether because they are losing business to private credit or because they are worried about the loans they’ve made to those funds—they stop lending to the real economy.

They stop lending to the couple buying their first apartment. They stop lending to the small garage owner who needs a new hydraulic lift.

The rise of private credit has created a two-tier system. If you are a massive private equity firm, you have access to a limitless pool of "shadow" money. If you are a regular person, you are stuck with a banking system that is increasingly defensive, guarded, and squeezed.

The irony is that much of the money in those private credit funds belongs to the public. It is the pension money of that same teacher and nurse. Their retirement is being bet on loans that have no public price, no regulatory oversight, and no easy exit strategy.

The Cracks in the Glass

We have been here before, though the names change. In 2008, it was subprime mortgages. In 2024 and 2025, the vulnerability is "corporate leverage."

The difference this time is the speed. In the old days, a bank failure was a slow-motion car crash. You could see the bad loans piling up on the balance sheet for quarters. Private credit is different. Because there is no public market for these loans, the value doesn't drop incrementally. Everything looks fine, at 100 cents on the dollar, until the day it's worth zero.

It is a "mark-to-myth" accounting system.

During this earnings season, watch the body language of the CEOs. Watch for the mentions of "non-bank financial intermediation." It sounds boring. It sounds like a textbook. It isn't. It is the sound of a tectonic plate shifting beneath the feet of the European economy.

The banks are no longer the only game in town, and that makes them desperate. Desperate banks make mistakes. They lower their standards to compete. They take risks they shouldn't. They try to "innovate" their way back to relevance.

The Empty Vault

The sun sets over the European Central Bank headquarters in Frankfurt, a twin-towered monument to the idea that money can be controlled, measured, and mastered.

But money is like water. It finds the path of least resistance. Currently, that path leads away from the regulated, lit hallways of the traditional bank and into the carpeted, quiet rooms of the private fund.

The earnings reports will show profits. They might even show growth. But look closer at the gaps between the lines. Look at the deals that aren't there. The story of European banking right now isn't what is happening inside the banks. It is what is happening in the silence outside of them.

We are participating in a massive, unvetted experiment in how much of a financial system can exist in the dark before someone trips over the furniture. The lights are on in the earnings calls, but the real activity is happening in the shadows, where the regulators can't see and the math is whatever the lender says it is.

The ghost is no longer at the feast. It has started eating the dinner.